Over $1.28 billion has flowed into African electric mobility companies since 2019, spread across 129 deals tracked through early June 2026 by TechCabal Insights. That number alone signals a shift, but the more telling detail is where the money is coming from. Debt now accounts for 34% of total funding, roughly $437 million, up from zero in 2019, and it actually overtook equity in 2023. Lenders do not move into a sector until its assets can be collateralised and its cash flows predicted.

Dieko Ojo, an investment associate at Novastar Ventures, puts it plainly: "Mobility financing businesses are debt-intensive by nature, and the ability to scale depends heavily on access to affordable and appropriately structured debt." That shift in capital type is matched by a shift in deal size. Since 2021, rounds of $10 million or more have captured at least three-quarters of annual funding. The market is no longer writing small cheques to test ideas. It is funding build-out.

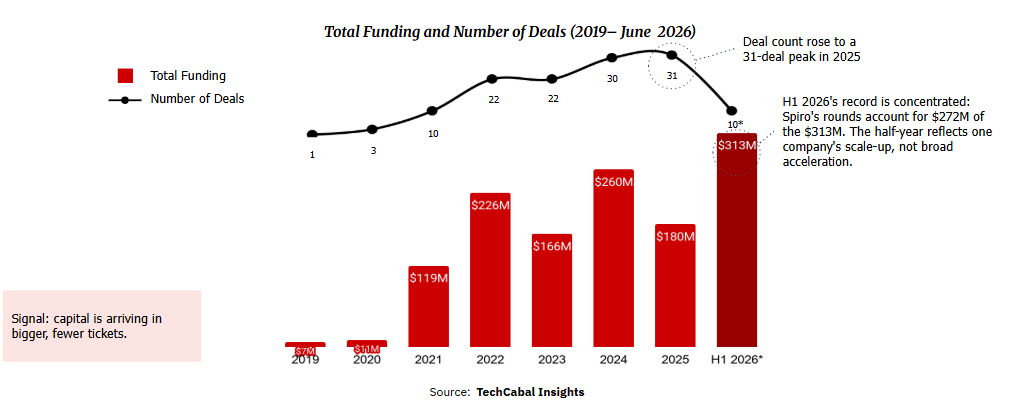

Annual figures have not moved in a straight line. Funding ran from $119 million in 2021 to $260 million in 2024, dipped to $180 million in 2025, then surged. The first half of 2026 alone brought in $313 million across just ten deals, more than the whole of 2025. One number in that figure deserves context: Spiro, the electric two-wheeler and battery-swap company, accounts for roughly $272 million of it. The half-year record reflects one company's scale-up, not a broad acceleration across the sector.

The African Development Bank is watching the same trend take shape. Wale Shonibare, the bank's director of energy financial solutions, policy and regulation, says AfDB's support for e-mobility operators is now conditional on three things: scalable and commercially viable business models, predictable revenue streams, and a supportive regulatory environment. To meet that moment, the bank is developing the Green Mobility Facility for Africa, a blended finance platform designed to mobilise more than $300 million through a mix of guarantees, commercial lending, and financial intermediation.

The companies building electric two- and three-wheelers, e-buses, battery-swap networks, and vehicle financing across the continent are starting to look less like startups and more like infrastructure operators. The question now is which markets and which models attract the next wave of that capital.

Originally published by TechCabal.